open banking,5 min read

How Open Banking is Changing SME LendingOpen banking transforms SME access to finance. With verified real-time financial data, brokers close deals faster and lenders make better credit decisions. Discover the statistics reshaping UK commercial finance.

| Open Banking Growth in UK | Figure |

|---|---|

| Active open banking users (March 2025) | 13.3 million |

| Year-on-year growth rate | 40% |

| SMEs actively using open banking | 750,000 |

| SME adoption penetration rate | 16% |

| Consumer adoption penetration rate | 11% |

| Open banking payments (July 2025) | 29.89 million |

| Market share of Faster Payments | ~8% |

The problem is simple.

SMEs struggle to access finance because lenders cannot verify financial data quickly. Brokers waste time requesting documents. Banks ask for bank statements, accountancy reviews, and historical records. The entire process moves slowly.

Open banking solves this.

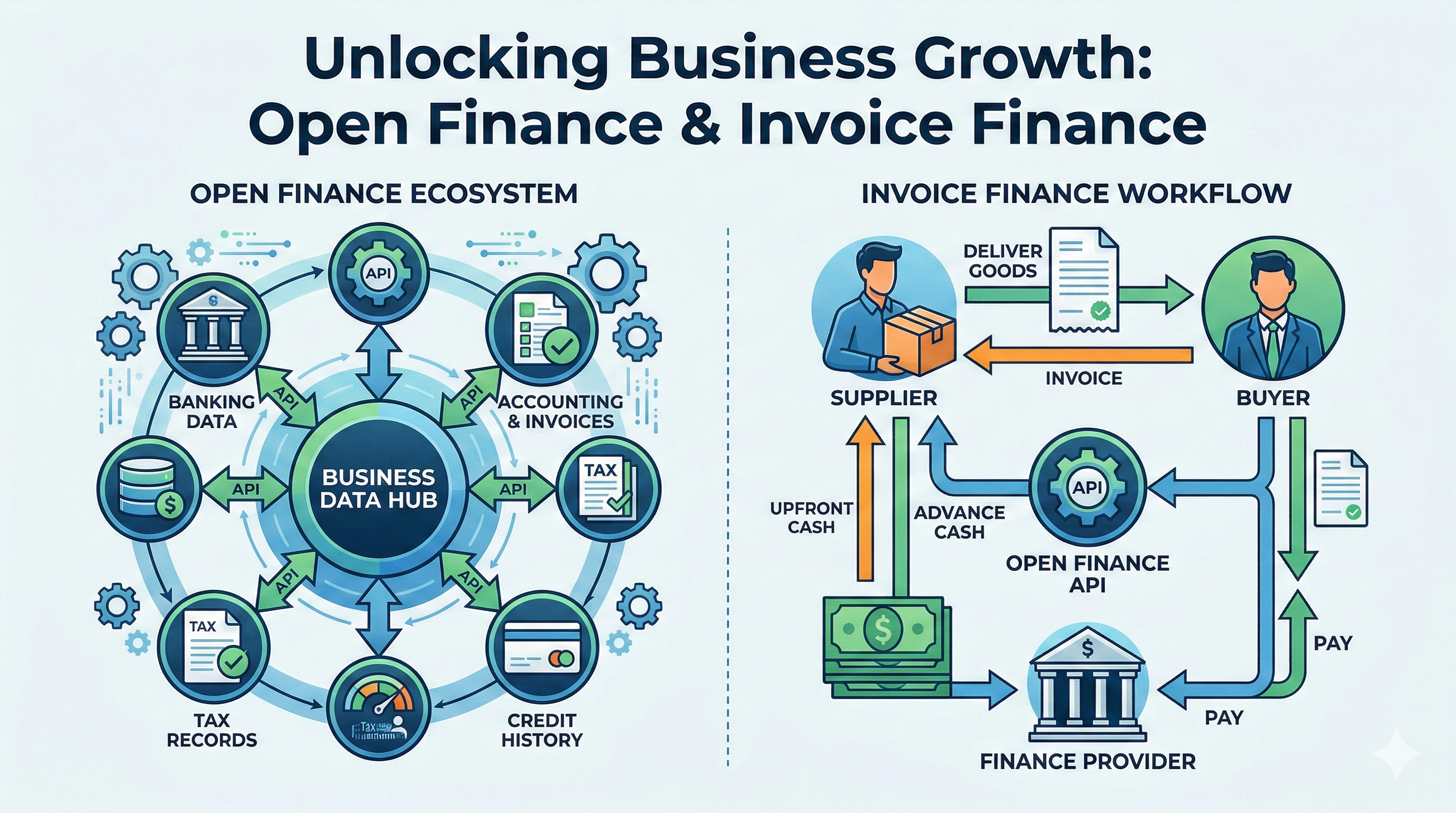

Open banking enables direct, secure access to verified financial data from SME bank accounts. Lenders gain real-time visibility into turnover, cashflow, and trading patterns. Brokers access the information instantly. SMEs receive funding decisions faster.

The shift is happening now. Over 750,000 SMEs actively use open banking products today. The adoption rate for businesses reaches 16% compared to just 11% for consumers. This gap widens monthly as more businesses realise the competitive advantage.

Open banking eliminates data friction.

Traditional SME lending relies on self-reported information. The SME owner provides a spreadsheet. The broker manually enters the data into multiple lender systems. Lenders conduct extensive due diligence to verify what should be straightforward information.

Open banking breaks this cycle.

Real-time account data flows directly from the SME's bank to lenders and brokers. The data arrives verified. It arrives complete. It arrives in standardised format ready for instant analysis.

This delivers three immediate benefits:

Instant financial visibility. Lenders see actual trading performance, not historical estimates. Turnover data arrives real-time. Cashflow patterns emerge instantly. Seasonal trading trends appear obvious.

Faster due diligence. Lenders process applications in days instead of weeks. They no longer chase missing documents. They conduct underwriting on complete, verified data.

Better credit decisions. With real-time cashflow data, lenders assess affordability accurately. They identify pre-arrears early. They detect financial stress before defaults occur.

| How Open Banking Changes Lending | Figure |

|---|---|

| Traditional process | Open banking process |

| Manual document request | Real-time data access |

| Self-reported financials | Verified bank data |

| Days to process | Hours to process |

| Incomplete applications | Complete applications |

| High rejection rates | Better matching rates |

The Financial Conduct Authority recognises open banking's potential to transform SME finance.

In March 2025, the FCA ran an Open Finance Sprint bringing together over 110 stakeholders. The sprint focused explicitly on how open finance data can improve SME lending outcomes.

Key datasets for SME lending included:

Accounting and tax information from accounting software systems.

Forecasts and operational records showing future trading expectations.

Real-time cashflow data enabling AI-driven alerts on financial stress.

The FCA now runs dedicated SME Finance TechSprints running through February 2026. These sprints test how open banking can genuinely improve funding access and speed lending decisions.

This regulatory commitment signals clear direction: open banking is the infrastructure for future SME lending.

Open banking delivers measurable real-world impact.

Salad Finance, an FCA-regulated lender, uses open banking data to approve loans for people traditional lenders reject. The platform serves individuals with invisible or inaccurate credit histories: young adults, people new to the UK, and the financially vulnerable.

In 2024, Salad's open banking integration identified £68.2 million in unclaimed benefits across customer accounts. This single finding changed outcomes for borrowers facing decline.

For many declined customers, that £68.2 million in identified benefits represented the difference between needing to borrow and accessing existing support. Average benefit recovery reached £2,300 per person annually.

This illustrates open banking's fundamental power: it reveals financial capacity hidden in traditional credit scoring.

SME adoption of open banking products exceeds consumer adoption.

16% of SMEs actively use open banking compared to 11% of consumers. This gap widens monthly and reflects business demand for operational efficiency.

Why the difference?

Business value is immediate and quantifiable. SMEs using cloud accounting software like Xero and Sage automatically connect to open banking systems. Transaction import becomes instant. Bank reconciliation requires no manual entry.

Funding access improves directly. SMEs implementing open banking access alternative finance faster. Broker research time compresses. Lender approval decisions accelerate.

Operational visibility enhances daily. Real-time cashflow data helps SME owners manage business finances actively. AI-powered alerts flag potential problems early.

| Consumer vs Business Adoption Rates | Figure |

|---|---|

| Consumer open banking adoption | 11% |

| SME open banking adoption | 16% |

| Adoption gap | 45% higher for businesses |

| Primary driver | Cloud accounting integration |

| Total SMEs using open banking | 750,000+ |

Open banking transaction volumes prove market maturity.

In July 2025 alone, open banking payments reached 29.89 million transactions. This represents roughly 8% of all Faster Payments processed in the UK. The UK open banking ecosystem processed 2 billion API calls in July 2025.

This scale demonstrates open banking has moved beyond concept. It now underpins material volumes of actual financial transactions.

For SME lending specifically, this payment infrastructure means data flows continuously. Lenders see updated financial information automatically. Fraud detection systems identify anomalies instantly.

Security concerns often dominate open banking discussions. The data contradicts concerns.

Open banking transactions demonstrate significantly lower fraud rates by volume compared to other payment types. This reflects multiple factors: customers actively authorise transactions; APIs enforce strict security protocols; standardised authentication prevents fraud entry points.

For SME lending, this security foundation matters enormously. Lenders confidently access real financial data. Brokers transmit sensitive information securely. SMEs retain control over data sharing with explicit consent mechanisms.

The FCA maintains robust oversight. All open banking participants comply with PSD2 security requirements. Banks and fintechs undergo regular conformance testing.

Open banking represents the foundation. Open finance builds on top.

Open finance extends data sharing beyond bank accounts. SMEs share accounting records. Tax information flows directly from HMRC. Pension data becomes accessible. Invoice records connect automatically.

For SME lending, this creates transformative possibilities:

Comprehensive financial visibility emerges from multiple sources simultaneously.

Credit decisions improve with data accuracy, completeness, and real-time updating.

Alternative lending products become possible with verified income and expense data.

Pricing reflects actual risk more accurately as data completeness improves.

The FCA's 2025 Open Finance Sprint outputs inform regulatory roadmap development through March 2026. The direction is clear: UK financial services moves toward comprehensive open finance.

Open banking has transitioned from regulatory requirement to competitive necessity.

750,000 SMEs actively use open banking today. That number grows weekly. The adoption rate for businesses reaches 16%, outpacing consumer adoption by 45%. Transaction volumes reach 2 billion API calls monthly. Payment volume hits 30 million transactions.

For SME funding specifically, open banking delivers measurable acceleration:

Lenders access verified financial data instantly instead of requesting documents for weeks.

Brokers complete applications in hours instead of days.

SMEs receive funding decisions days faster with complete, verified information.

Credit decisions improve with real-time data accuracy.

The FCA doubles down on this direction. SME Finance TechSprints test practical applications through February 2026. Regulatory frameworks align with open banking implementation.

This is why FundingSearch integrates open banking APIs. Verified financial data from bank connections replaces manual document requests. Real-time information replaces self-reported figures. Intelligent matching leverages complete financial visibility.

Open banking removes friction from SME funding. Brokers work smarter. Lenders decide faster. SMEs access capital quicker.

Resource: https://www.openbanking.org.uk/how-open-banking-can-help-businesses/