open banking,5 min read

How Open Banking is Changing SME LendingThe UK's commercial finance industry stands at an exciting moment. The FCA's Open Finance Sprint 2025 has laid out an ambitious vision for 2030. The CFIT SME Finance Taskforce has identified critical barriers holding back Britain's 5.5 million small businesses. Now comes the collaborative work of turning regulatory vision into practical solutions.

As we prepare to participate in the FCA's SME Finance TechSprint this month, I wanted to share how FundingSearch is contributing to this important regulatory innovation agenda.

Two major regulatory reports published in 2025 have confirmed what commercial finance brokers have known for years. The system is broken. More importantly, they've outlined exactly how to fix it.

The FCA's Open Finance Sprint 2025 Outcomes Report brought together over 110 stakeholders in March 2025. Their conclusion was unequivocal. Future SME lending must be built on "available, portable, and standardised" data. It must leverage "AI-driven analysis, agentic AI, and strong digital identity verification solutions". It must deliver "real-time insights and proactive services" supported by "enhanced common APIs standards".

The CFIT report Smart Data: Improving SME Lending to Drive Economic Growth went further. It quantified the problem. Bank lending to SMEs has fallen 20% in real terms since 2014. Over 50% of declined applicants never seek alternative lenders. Brokers waste 20+ hours per deal on manual lender research.

Both reports arrive at the same solutions. Verified financial data from accounting software providers. Digital integration with HMRC and Companies House. Intelligent matching platforms that reduce friction. Standardised APIs that enable automation.

As someone who has spent a decade as a commercial finance broker, these challenges aren't theoretical to me. They're problems I've tackled with every deal. This experience has informed how we've built FundingSearch to contribute to the solutions regulators have identified.

I built FundingSearch because I experienced these inefficiencies first-hand. Every deal meant manually researching hundreds of lenders. Every application required compiling data packs from fragmented sources. Every declined client represented a missed opportunity, knowing better options existed somewhere in the market.

The FCA's Vision 2030 describes five foundational pillars. Our work at FundingSearch explores how technology can support each one.

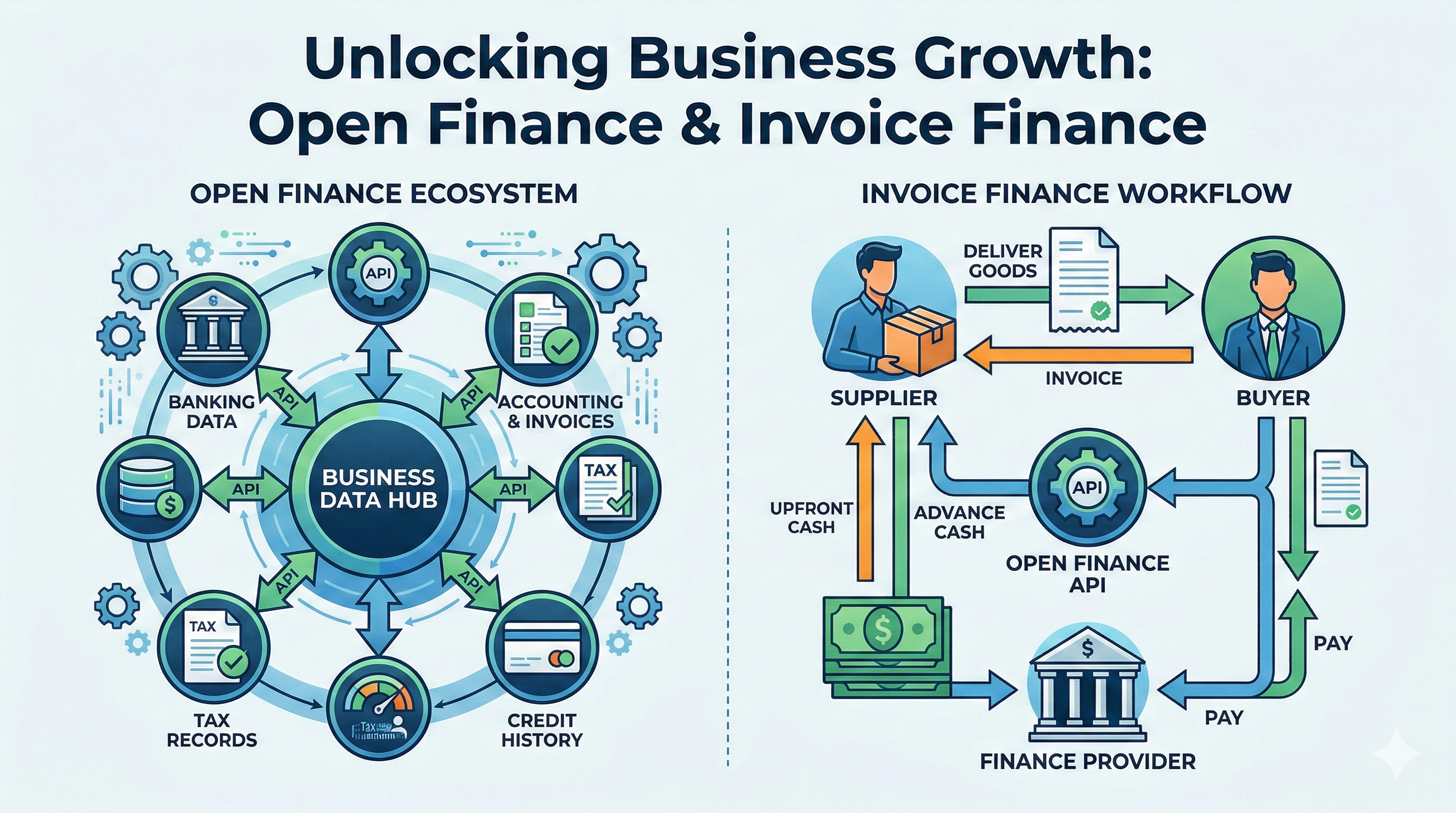

The CFIT report identifies access to cloud accounting data as critical for unlocking SME finance. Lenders need "up-to-date financial information held in cloud accounting software by providers such as Sage, Xero, Intuit QuickBooks".

Our approach integrates directly with Xero and Sage. Live P&L, balance sheet, and cash flow data can pull automatically. This reduces reliance on PDFs and manual data entry. It's our contribution to what the FCA envisions when describing "secure and reusable digital IDs, digital wallets and machine-learning models capable of assessing both traditional and non-traditional financial signals".

The CFIT report found that traditional lenders using proprietary data consistently outperform newer lenders lacking this access. Our platform aims to help level this playing field by providing verified data to brokers and their lender panels.

The FCA sprint highlighted "AI-driven tools fed by data shared securely using open finance could support consumers in navigating complex decisions". The CFIT report revealed that 50% of declined SMEs never approach alternative lenders.

Our matching algorithm generates ranked lists of suitable lenders from business profile data. Match probability scores include reasoning. This addresses the problem both regulators identify - SMEs lack understanding of the finance market, and brokers need more efficient research tools.

We're working to reduce research time significantly, targeting the efficiency gains the CFIT report highlights as necessary for the industry.

Both reports emphasize digital identity as "a critical enabler, facilitator or catalyst of open finance". The FCA describes "secure, streamlined access to services" through verified credentials.

Our Companies House auto-lookup feature provides business verification. Directors are confirmed. Company structure is validated. This helps address what the CFIT report identifies as a major friction point - Companies House data currently exists in "PDF format which is difficult to absorb digitally" with "lack of standardisation in naming conventions".

We're exploring how technology can improve this verification process whilst we await broader Companies House reforms.

The CFIT report calls for "technical standards that fit alongside the data" and "conformance services to ensure quality implementation". The FCA envisions "standardised, high-quality data through shared infrastructure".

Our master application architecture allows SMEs to input data once, with smart field mapping distributing information to multiple lender forms. This approach aims to reduce application completion time significantly, working towards the "modular consent and personalisation layers built on shared infrastructure" the FCA describes.

As industry standards evolve, we're committed to ensuring our platform aligns with emerging best practices.

The FCA sprint identified SME finance as requiring diverse datasets. The CFIT report notes that different finance types need different data. Asset finance needs asset registers. Invoice finance needs invoice data. Working capital needs cash flow projections.

Our platform covers the full commercial finance spectrum - asset finance, invoice finance, working capital, trade finance, merchant cash advance, and property finance. Each product type aims to connect with relevant verified data sources as they become available through regulatory initiatives.

We're learning what data combinations work best for different lending scenarios, insights we'll share through the FCA's TechSprint process.

Both regulatory reports identify specific data sources as essential. We've mapped our current development against their recommendations to understand where technology can contribute today and where regulatory reform is needed.

| Data Source | CFIT Priority | FCA Vision 2030 | FundingSearch Progress |

|---|---|---|---|

| Cloud accounting (Xero, Sage) | High - "directly access to up-to-date financial information" | Core enabler - "comprehensive understanding of consumer's finances" | Active integration - P&L, balance sheet, cash flow |

| Companies House verification | High - "verify directors and standardised naming" | Foundation - "digital identity verification solutions" | Built - auto-lookup, verification workflows |

| Bank transaction data | High - "reconciliation of management accounts" | Essential - "transaction histories" as core dataset | Ready - Open Banking compatible architecture |

| VAT submissions | High - "reliable indicator of revenue" | Verification layer | In development - through accounting software integration |

| Credit reference data | High - "multiple information streams" | Risk assessment foundation | Planning - CRA connections in roadmap |

| Invoice data | Medium - "reconciliation difficult" | Growth opportunity - "business track records" | Planned - Q2 2026 rollout |

This mapping shows where we can contribute with existing technology and where we need regulatory progress. Both are essential for the industry transformation both reports envision.

The CFIT report quantifies the urgency. Bank lending to SMEs in 2024 sits £10 billion below 2014 levels in real terms. This represents missing jobs, missing innovation, missing growth.

The FCA identifies four opportunity areas where open finance can transform outcomes. Financial wellbeing. Financial growth. Financial resilience. Digital identity. Our work at FundingSearch explores practical applications in each area.

Financial wellbeing: Technology can help flag risks before they arise. Brokers can see cash flow gaps early. SMEs can receive options based on verified affordability.

Financial growth: Intelligent matching can surface growth opportunities. SMEs can discover lenders they never knew existed. Brokers can access specialist products more efficiently.

Financial resilience: Real-time data can enable faster interventions. When cash flow tightens, alternative funding options can appear more quickly. The 50% who currently give up after one decline might find new paths forward.

Digital identity: Companies House integration and accounting software verification can create more trusted business profiles. These could become portable across lenders, working towards the "single, verified identity across platforms" the FCA describes.

These opportunities require collaboration between technology providers, regulators, lenders, and brokers. No single platform solves everything, but each contribution moves the industry forward.

FundingSearch is participating in the FCA's SME Finance TechSprint this month. This initiative sits within the Smart Data Accelerator programme. Its purpose is testing high-impact use cases, enabling agile policy development, and identifying suitable data and technology infrastructure needs.

We're participating to contribute our practical experience to the regulatory innovation process. As a broker-built platform, we understand the real-world challenges from both sides of the market. We're eager to learn from other participants and help the FCA understand what works, what doesn't, and where regulatory support is most needed.

The FCA's sprint outcomes report describes testing as moving "from ideation to implementation". We hope our participation can provide useful insights on this journey. Our experiences with data integration, broker workflows, and lender requirements might help inform the practical policy development the FCA is undertaking.

More importantly, we're keen to learn from the wider ecosystem. Other TechSprint participants will bring different perspectives, different technologies, and different approaches. This collective learning is how the industry moves forward together.

The CFIT report delivers seven immediate action points for unlocking SME finance. Technology platforms like FundingSearch can contribute to six of them in practical ways.

1. Prioritise the Digital Information and Smart Data Bill

Our platform architecture is designed for smart data integration. Our APIs can work with cross-sector data sharing. Our consent frameworks aim to align with emerging standards. We're ready to adapt as new regulations emerge.

2. Fund and support an SME "Smart Data Challenge"

Our experience testing these technologies in a real broker environment provides useful data points. We can demonstrate what works in practice, what challenges emerge, and where more development is needed.

3. Review and improve Bank Referral and Commercial Credit Data Sharing schemes

Our marketplace approach offers one model for how improved referrals might work. We don't claim it's the only answer, but hope our experience can inform the review process.

4. Accelerate Companies House reform

We've built verification workflows that work with current data. When Companies House standardises director names and provides better API access, we're ready to integrate these improvements quickly.

5. Unlock HMRC data access

Our accounting software integration creates one potential bridge. When HMRC opens digital VAT receipts, platforms like ours can help verify this data against accounting records, supporting the validation lenders need.

7. Enable greater trust in specialist lenders

Our platform aims to help brokers vet lenders whilst maintaining independence. We don't force AR networks or commission splits. This preserves broker discretion whilst improving access to verified lenders.

Each of these contributions is part of a broader industry effort. No single platform provides all the answers, but collective innovation moves us closer to the vision both regulatory reports describe.

Both regulatory reports emphasise sustainable commercial models. The FCA describes "aligned incentives, flexible revenue-sharing arrangements and value distributed across all actors in the ecosystem". The CFIT report warns against models that reduce competition.

Our approach preserves broker independence. We don't require AR network membership. We don't split commissions. We don't force exclusive lender relationships.

Brokers maintain their existing lender connections. They keep full commission structures. They gain efficiency tools without sacrificing autonomy.

This model aims to align with the FCA's vision of "interoperability and cross-sector collaboration to create a cohesive and organic financial ecosystem". It works towards what the CFIT report identifies as essential - reduced friction without consolidated control.

Whether this proves to be the right model will emerge through market testing. We're committed to adapting based on broker feedback and regulatory guidance.

I built FundingSearch in Sheffield - not London, not a fintech hub, but a real city where real businesses face real financing challenges.

The CFIT report notes that SMEs employ 16.7 million people across the UK. They generate over half of UK business turnover. Their success matters to communities across the entire country.

The FCA's Vision 2030 describes "a sector in which finance is open, secure, intelligent and highly personalised, all powered by proactive regulation, intelligent technology and innovation". Achieving this vision requires practical tools that work for brokers and businesses everywhere, not just in financial centres.

Every SME that gives up after one decline represents an opportunity to improve. Every broker who spends 20 hours on manual research highlights where technology can help. Every lender who receives incomplete applications shows where better data infrastructure is needed.

These aren't just statistics. They're the daily reality that informed how we built our platform.

The FCA commits to publishing an open finance roadmap by March 2026. This roadmap will set policy direction, define regulatory frameworks, and establish standards.

We're committed to aligning with these developments. Our technology can adapt to new requirements. Our data integrations can expand as new sources become available. Our broker community provides ongoing feedback on what works in practice.

The CFIT report concludes with urgency: "There is no time to waste." We agree. That's why we're actively participating in the FCA's innovation agenda whilst continuing to develop practical tools that help brokers today.

The commercial finance industry needs both regulatory reform and technology innovation. We need government to unlock HMRC data. We need Companies House to standardize verification. We need industry collaboration on data standards.

Technology platforms like FundingSearch can contribute to this transformation, but we're one piece of a larger puzzle. The real progress comes from regulators, lenders, data providers, brokers, and technology companies working together.

What's needed isn't just capability. It's sustained collaboration.

We're ready to contribute our part.

Key Regulatory Evidence Summary

FCA Open Finance Sprint 2025 Outcomes Report (July 2025)

CFIT SME Finance Taskforce Report (August 2024)

FundingSearch's Contribution to the Vision

FundingSearch is working to support the regulatory vision through:

We're contributing our practical experience to help shape industry innovation whilst learning from regulators, lenders, and fellow technology providers.